The Southeast Asian (SEA) electronics market is currently undergoing a fundamental structural transformation. For years, the region’s growth story was one of pure volume—more smartphones, more laptops, and more entry-level appliances in the hands of a rapidly digitalizing population. However, the data for 2025 reveals a decisive pivot: the market is moving from "buying more" to "buying better".

Throughout 2025, a clear Premiumization Paradox has emerged. While unit volumes in some categories are softening, the total value of the market is surging, driven by a middle class that is increasingly willing to trade up for feature-rich, modern, and high-efficiency devices.

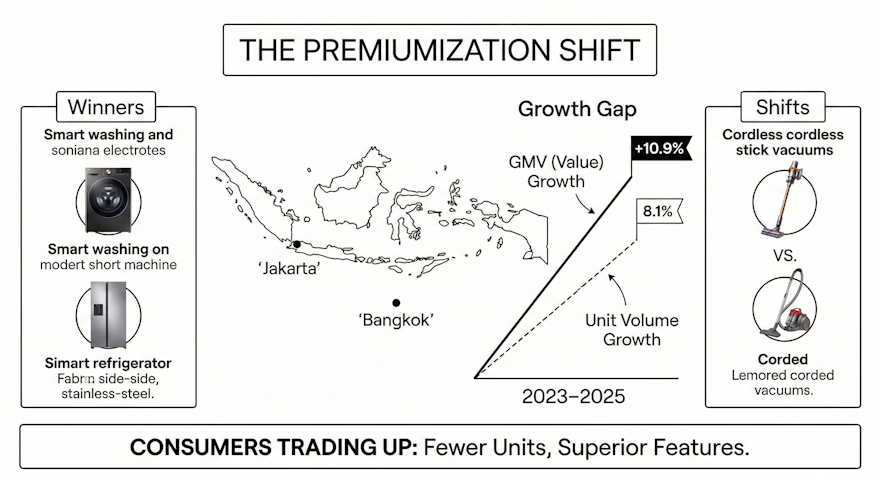

The Growth Gap: Trading Up, Not Just Buying More

The most striking evidence of this shift lies in the divergence between quantity and value. Regionally, Gross Merchandise Value (GMV) is expanding at a healthy 10.9%, significantly outpacing unit growth, which sits at 8.1%.

This "Growth Gap" signals a "trading up" phenomenon. Consumers are no longer just entering the digital economy; they are maturing within it. Stabilization in inflation across many parts of Emerging Asia has helped consumers move from cautious to "intentional" spending. Rather than big-ticket splurging on any available item, shoppers are looking for "Affordable Premium"—mid-tier devices that offer high-end features and modern designs at accessible price points.

The Efficiency Play: Winning on Value, Losing on Volume

For major players in the region, 2025 has become a year of "Efficiency Gains." Leading brands are reporting a unique performance profile: massive revenue growth (upwards of +24.6%) occurring even as their total unit volumes dip (approximately -5.7%).

This confirms a critical market reality: Profit now lies in the premium mix. The era of aggressive volume-chasing at the expense of margins is being replaced by a strategy focused on higher Average Selling Prices (ASP). For instance, the average price of electronics in the region has climbed to $54.25, a 2.6% increase that reflects a move toward more expensive, feature-led models.

Sector Winners: The Rise of Major Appliances

The demand for electronics is not shifting uniformly. We are seeing a polarization between "High-Growth Stars" and "Sunset Plays".

Major Appliances (The Growth Engines): Demand is heavily concentrated in high-ticket items like Refrigerators and Washing Machines. These categories are delivering strong momentum in both volume and value as urbanization grows and new housing creates a functional need for home upgrades.

Legacy Formats (The Structural Decline): Conversely, legacy small appliances are facing a harsh reality. Vacuum Cleaners, in particular, are in structural decline. The market is rapidly moving away from bulky, corded canisters toward cordless stick models and handheld formats. Consumers are essentially trading traditional functionality for convenience and portability.

Market Spotlight: The Two Faces of SEA Growth

The region's growth is being spearheaded by two distinct leaders, each representing a different side of the electronics boom:

1. Indonesia: The Scale Driver

Indonesia remains the undisputed engine of volume in Southeast Asia. It contributes the largest unit base and continues to see the strongest volume expansion. With a tech-savvy population and rising disposable incomes, the Indonesian consumer electronics market is projected to grow at a CAGR of approximately 8.5% through 2025. Government initiatives to boost local manufacturing and digital infrastructure—including a roadmap for domestic semiconductor production—are further cementing Indonesia's role as the region's scale leader.

2. Thailand: The Premiumization Leader

While Indonesia leads in scale, Thailand has emerged as the region's premiumization leader. It boasts the highest average prices, driven by a sophisticated consumer base that prioritizes upgrades over first-time purchases. In the Thai market, demand for OLED, QLED, and ultra-large-screen TVs is expected to drive a 2% growth in the TV sector alone, even as general spending power remains tight. This "Smart Electronics" segment is supported by strong domestic investment and a shortened replacement cycle—shaving years off the typical time a consumer holds onto a device.

The Path Forward: How to Win in 2025

For brands and retailers, the 2026 landscape requires a move away from "one-size-fits-all" regional strategies. Success now depends on:

Prioritizing Portability and Convenience: In categories like blenders and vacuums, corded and bulky is "out"; cordless and multi-functional is "in".

Syncing with Mega-Campaigns: E-commerce data shows that missing the peak of a mega-campaign (like 11.11 or 12.12) by even one month can lead to permanent share loss, as consumers are no longer willing to wait for stock.

Building a Clear Pricing Ladder: Brands must balance "controlled entry-tier" models to protect volume with "feature-led upgrade" models to capture the premium shift.

The SEA electronics market is no longer a simple volume play. It is a nuanced, value-driven arena where the winners are those who can provide the "premium feel" at an "affordable" price point, all while maintaining a razor-sharp focus on the shifting lifestyles of the modern Asian consumer.

Stay ahead of competitors and protect your brand equity. Request a demo with MagpieIQ today to unlock market share insights tailored for your business.