The prevailing read across the region's ecommerce analysts — one we largely share — is that TikTok Shop spent 2025 closing an enormous amount of ground on Shopee, powered by live selling and content commerce. According to Magpie IQ data, that holds up year-on-year: TikTok Shop's Indonesian channels grew strongly through 2025. What our more recent monthly data adds to the conversation is a category-specific signal that has emerged since January 2026 — and a plausible operational explanation for it. We are scoping this piece to beauty and personal care deliberately, because that is where Magpie IQ's SKU-level tracking in Indonesia is deepest and most consistent.

Where the conversation stands — and what fresh data can add

There is broad, well-earned agreement in the industry that Indonesia's platform race narrowed sharply in 2025. TikTok Shop's integration with Tokopedia gave it scale, live commerce shifted discovery away from search, and the annual figures published this spring captured a market growing faster than it had in years. Magpie IQ's own tracking agrees with the direction of travel: measured over the full year, TikTok Shop was the fastest-growing way to sell in Indonesia.

That story is now well-documented. The question worth adding to — the one annual figures cannot answer — is what happens after the calendar year closes. This is where continuous, SKU-level tracking earns its keep, and where we think Magpie IQ can make a useful contribution rather than restate what is already known.

We are keeping the lens on one category: beauty and personal care. It is the right place to look for two reasons. First, it is widely understood to be TikTok Shop's single largest category by GMV — the natural home of the demo-friendly, live-selling format — so it is where the platform's momentum should be most durable. Second, and just as important, it is the Indonesian category where Magpie IQ's coverage is deepest: tens of thousands of tracked beauty SKUs across platforms, month after month. When we make a claim here, we can stand behind the granularity. That is a deliberately narrower scope than a whole-market call, and we would rather be precise than sweeping.

What Has Happened in Indonesian Beauty Since January 2026?

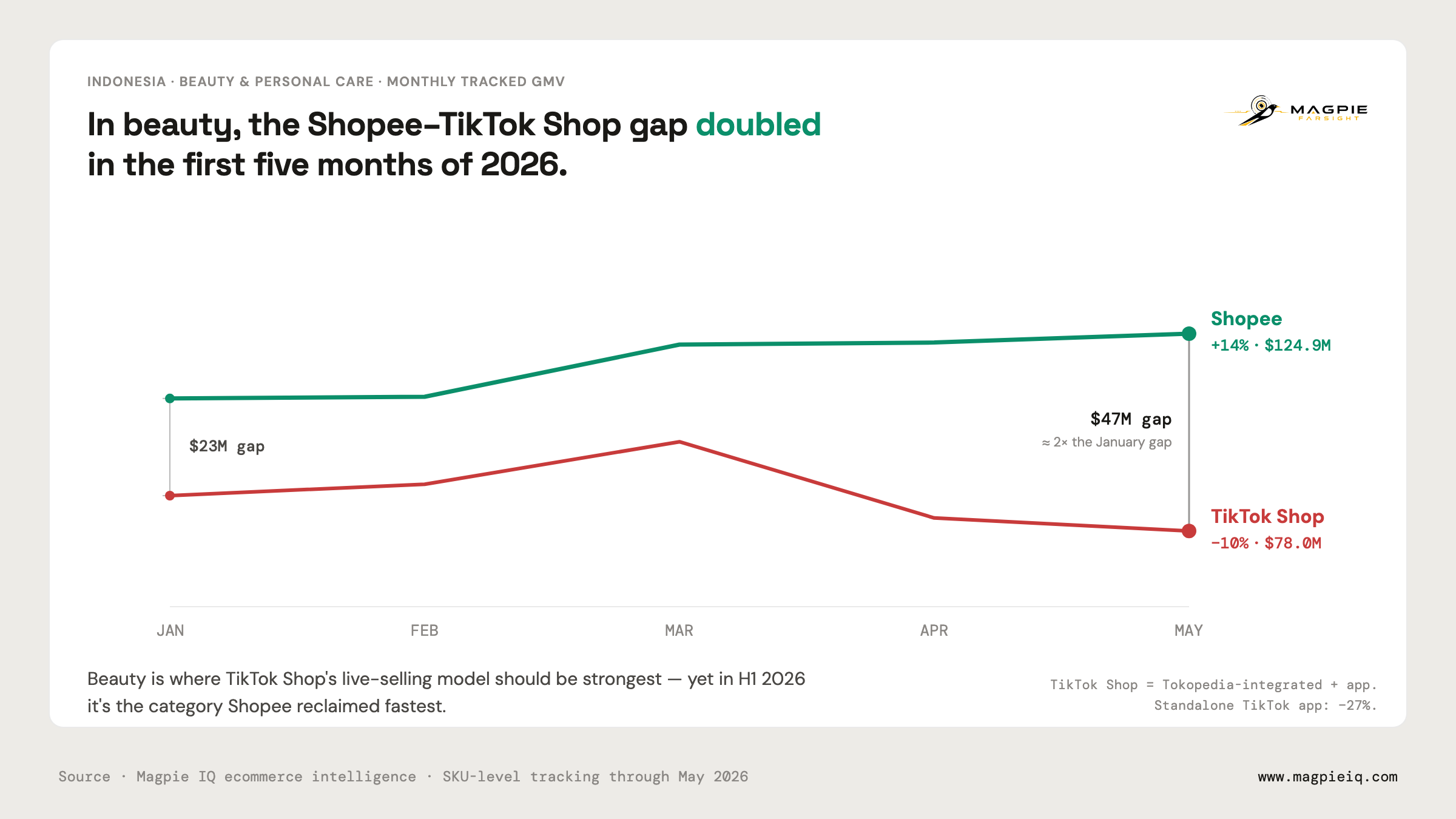

The gap between the two leading ways to buy beauty online has widened — and it has done so steadily, not in a single jump. According to Magpie IQ data, Shopee's tracked beauty and personal care GMV in Indonesia rose from US$109.5 million in January 2026 to US$124.9 million in May — up 14%, climbing in every one of the five months. Over the same window, TikTok Shop's beauty GMV (its Tokopedia-integrated storefront and standalone app combined) fell about 10%, from roughly US$86.4 million to US$78.0 million. The standalone TikTok app channel fell further, down 27%.

Put those two lines together and the story is the gap. In January the two platforms were about US$23 million apart in tracked beauty GMV. By May the distance had grown to about US$47 million — roughly double, in five months.

Two honest caveats keep this grounded. December is always the seasonal peak, inflated by year-end mega-campaigns, so every platform steps down into January; the useful signal is the shape of the months that follow, not the holiday cliff. And the March uptick visible on both platforms lines up with Ramadan and Lebaran demand. Neither changes the underlying pattern: Shopee climbed consistently after the seasonal reset, while TikTok Shop recovered only briefly before easing back below where it started the year. The brand panel behind these figures is stable month to month — Magpie IQ tracks beauty across roughly 11,500–12,000 brands on Shopee and about 5,200 on the TikTok app in Indonesia each month — so this reflects a genuine shift in what is selling, not a change in what we measure.

Is This a Reversal — and Why Might It Be Happening?

The intellectually honest answer to the first question is: it is an inflection worth watching, not a collapse. TikTok Shop remains, by a wide margin, the second force in Indonesian beauty, and its year-on-year growth is still positive. Nothing in five months of data undoes a breakout year. What the monthly view surfaces is that the rate of gaining has turned in the one category where it should be most secure — and that is a signal a category manager would want on their radar early, not in an annual review two quarters from now.

As for why, one explanation is consistent with something already public. Through 2024 and 2025, TikTok Shop consolidated its Indonesian workforce following the Tokopedia merger — from a combined headcount of around 5,000 at the time of the deal to a reported 2,500, with reductions spanning operations, marketing and logistics, per People Matters. A leaner local organisation is a reasonable thing to connect to a category that runs on hands-on seller and creator enablement: beauty live-selling is operationally intensive, and it depends on the kind of on-the-ground merchant support that a thinner team is harder pressed to sustain.

We want to be clear about what this is: a hypothesis, not something the GMV data proves. Magpie IQ tracks what sells, not staffing decisions, and correlation in timing is not causation. But it is a plausible, testable read — and offering it is more useful to the conversation than presenting a number with no attempt to explain it. If the softening continues into the second half of 2026, the workforce explanation gets more credible; if beauty re-accelerates on TikTok Shop, it does not.

What This Means for Beauty Brands

Three implications, each anchored to the data above.

1. Re-check your own beauty numbers monthly, not annually. This category turned inside a single quarter, per Magpie IQ data; a channel mix set on 2025's full-year story could already be a step behind what buyers are doing in 2026. The brands that caught this shift are the ones watching month by month.

2. Shopee is the beauty surface currently adding share — invest there accordingly. Shopee grew its tracked beauty GMV 14% in the first five months of 2026 while the category's centre of gravity was assumed to be moving elsewhere. Official Store discipline on the platform that is actually growing is the low-drama, high-return move.

3. Keep your live-selling and creator engine close to home. If TikTok Shop's local support is thinner than it was, the beauty brands most insulated are the ones that own their creator relationships and live-selling operation rather than leaning on platform-run enablement. Build the muscle in-house so a shift in any one platform's support model does not move your whole funnel.

About the Data

Magpie IQ is an Indonesian ecommerce intelligence company that has tracked SKU-level sales data across Shopee, Tokopedia, TikTok Shop, Lazada, Blibli and Bukalapak continuously since 2021 — one of the longest and most granular longitudinal ecommerce datasets in Indonesia. This analysis is scoped to beauty and personal care in Indonesia, where our SKU coverage is deepest and most consistent; we hold other categories to the same evidentiary bar before publishing on them.

Sales Value (GMV) is calculated as final post-discount price × units sold (Terjual), with price held constant at the latest snapshot within the reporting period. TikTok Shop is measured across both its Tokopedia-integrated storefront and its standalone app channel; TikTok Shop data spans Q1 2025 onward, so single-platform year-on-year comparisons before that point are not directly comparable. The workforce figures referenced above are drawn from public reporting, not Magpie IQ's dataset, and the connection we draw to category performance is offered as a hypothesis, not a proven cause.

All Magpie IQ analysis is provided for informational purposes only and is presented as-is without warranties of any kind. Magpie IQ makes no representations as to the completeness or accuracy of third-party figures cited herein and accepts no liability for any decisions made in reliance on this article.

The Broader Picture

-

Southeast Asia's platform ecommerce reaches US$157.6B in 2025 — Momentum Works

The definitive full-year-2025 baseline for the region's platform race — excellent context for the annual story our monthly beauty data sits on top of.

-

Shopee, Lazada and TikTok Shop in Southeast Asia: what the data shows in 2026 — Cube Asia

A thorough regional read on TikTok Shop's 2025 acceleration, including beauty's role as its largest category — the wider picture this category-level view complements.

-

Is TikTok Shop gearing up for job cuts in Indonesia? — People Matters

The reporting behind the workforce-consolidation context we reference as a possible explanation for the beauty softening — offered here as a hypothesis, not a proven cause.

-

TikTok Shop narrows the gap with Shopee in Southeast Asia — KrAsia

A useful reminder that these dynamics are country- and category-specific: the gap is still narrowing in some markets even as Indonesian beauty diverges.